Overlooked Recession Signals

Headlines tout a drop in recession fears, with odds having fallen sharply from 70% just over a year ago. But a deeper look at the data reveals those risks are quietly rising again. And since a recession can hit retirement savings hard, now’s the time to take the warnings seriously and prepare.1

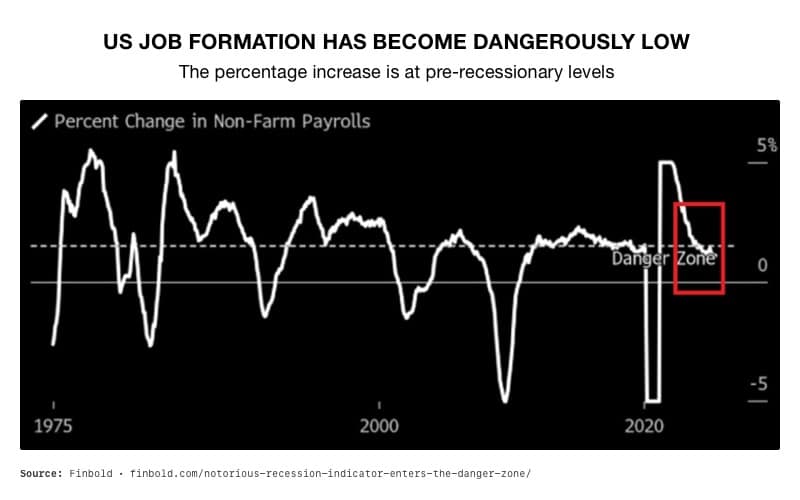

Labor Market Weakness Signals Deeper Trouble

For months, the labor market has been hailed as the pillar of economic resilience. But recent data from the Bureau of Labor Statistics paints a more troubling picture. Non-farm payroll growth has remained under 1.15% for four consecutive months. That is the weakest stretch since before the 2020 downturn. Historically, similar patterns have signaled recession.2

In fact, comparable declines in payroll growth occurred before recessions in the early 1980s, 1990s, 2001, and 2008. Even during the 1980s double-dip recession, job growth was stronger than it is today.

3

Housing Market Turns from Growth Engine to Drag

Chief Economist Mark Zandi of Moody’s Analytics has sounded the alarm on the housing market. After issuing a yellow warning in prior months, Zandi has now issued a red alert. He points to high mortgage rates hovering near 7%. They have begun to suppress demand, stall new construction, and pressure home prices.

Homebuilders, often the first to see trouble ahead, are already delaying land purchases. That typically signals a downturn in future sales, starts, and completions. Housing was a key driver of the post-pandemic recovery.

But if these trends continue, the housing sector could become an economic drag heading into late 2025 and early 2026. According to Zandi, “Housing will thus soon be a full-blown headwind to broader economic growth, adding to the growing list of reasons to be worried about the economy’s prospects later this year and early next.”4

Consumer Spending Cracks Are Widening

Consumer spending makes up roughly 70% of the U.S. economy. Which means even slight declines can have ripple effects. According to economic data, discretionary spending on services is already falling. Wells Fargo analysts say that’s a red flag. Historically, this metric has only declined during or immediately after recessions.

They noted that consumer spending data has been revised much lower than previous estimates. Even spending on goods, which appeared stable, is showing signs of weakness.

In the first quarter, Personal Consumption Expenditures (PCE) grew by just 0.5%. A stark drop from 2.8% in 2024. Wells Fargo also suspects that inflation might be understated due to delayed price increases stemming from tariffs.5

Trade Tensions Stir Recession Fears

Back in April, recession concerns spiked when U.S. trade tensions escalated. Though expectations eased following new trade agreements, fresh tariff deadlines are on the horizon. If those deals fall through, economic uncertainty could increase once again.

At the beginning of the tariffs, companies stockpiled goods, inflating imports and driving down GDP. In fact, the U.S. Bureau of Economic Analysis reported that GDP growth dropped 0.5% in the first quarter of 2025. Marking the first quarterly decline in two years.

Federal Reserve Caught in a Bind

The Federal Reserve’s latest projections are telling. In its June 2025 statement, the Federal Open Market Committee downgraded its GDP growth forecast. While also increasing projections for unemployment and inflation. Yet despite signs of slowing growth, the Fed remains committed to fighting inflation. And that may prevent it from cutting rates anytime soon.

This opens the door to a more dangerous scenario: stagflation. That’s when inflation remains high while the economy stagnates. Rob Haworth, Senior Investment Strategy Director with U.S. Bank Asset Management Group, put it simply: “If the economy experiences both rising inflation and higher unemployment, the Fed doesn’t have tools to address those concerns simultaneously.”6

Recession Risks Remain Elevated

While the probability of a recession has dipped below 50%, Zandi warned the risks remain elevated. According to Moody’s machine learning model, the probability of a recession within the next 12 months still stands at 45%. The combination of a softening labor market, stalling housing sector, falling consumer spending, and trade-related uncertainty adds up to this troubling outlook.7

And the numbers may be worse than they appear. The job market data doesn’t account for future revisions. Which means job growth may be even slower than currently reported. If these trends continue, a recession in late 2025 or early 2026 seems increasingly likely.

How a Recession Could Impact Your Retirement

For retirees and those nearing retirement, a recession can bring serious financial setbacks. Market declines can shrink retirement accounts, while lower interest rates may reduce income from investments. Inflation can erode purchasing power, and needing cash during a downturn might mean selling assets at a loss. Even part-time work, often relied on in retirement, can become harder to find.

Conclusion

Don’t get caught off guard. Despite the headlines, a recession remains a real risk. Faltering job numbers, a weakening housing market, and growing uncertainty from trade tariffs are all early warning signs. Now is the time to act. Physical gold, held in a Gold IRA, offers a time-tested way to protect the value of your savings from the potential impact of a downturn.

Call American Hartford Gold today at 800-462-0071 to learn how to safeguard your retirement with physical gold.