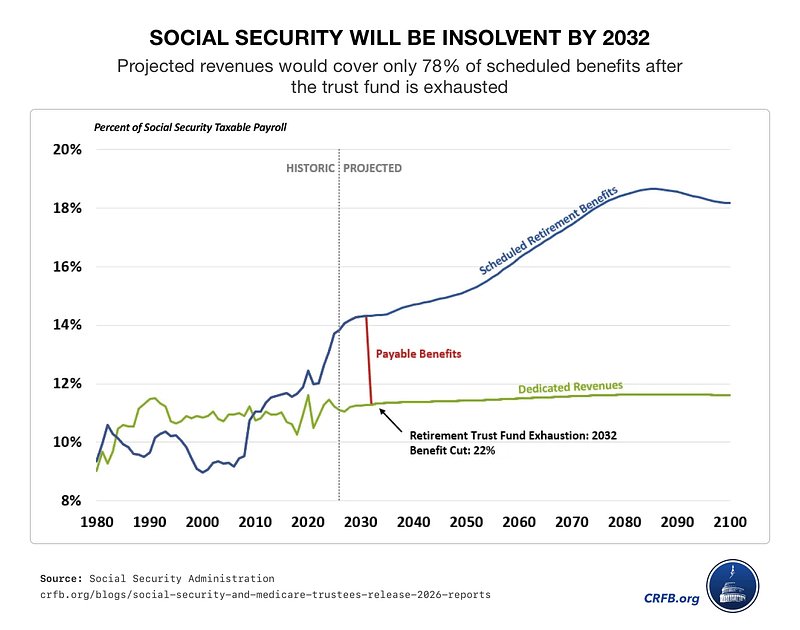

- Social Security’s main trust fund is projected to pay full benefits only until late 2032.

- Without congressional action, retirees could face benefit reductions of 17 percent to 22 percent.

- A Gold IRA can help protect your finances from inflation, uncertainty, and reduced government benefits.

The Social Security Shortfall

For decades, the looming Social Security funding gap felt like a distant problem. It was something future Congresses would eventually sort out. But the 2026 Trustees Report turned that distant concern into a dated deadline. Social Security’s main trust fund will pay full benefits only until the fourth quarter of 2032. After that, payroll tax revenue would cover just 78 percent of scheduled benefits. Myechia Minter-Jordan, CEO of AARP, put it plainly: “This should be a wake-up call: Congress needs to act.”1

With possible benefit cuts now measured down to the percentage point, retirees and near-retirees may need more than passive optimism. They may need to build more protection into their retirement.

A Dated Retirement Risk

The shortfall has become a dated, measurable event. The Old-Age and Survivors Insurance Trust Fund is projected to run short in 2032. If the retirement and disability funds were combined, the deadline would move to 2034. Even then, the system would have enough revenue to pay only 83 percent of promised benefits.

Retirees could face a reduction of 17 percent to 22 percent unless lawmakers reach a deal. Benefit checks would continue, but the amount would fall to match incoming revenue.2

The country has faced a similar moment before. In 1983, bipartisan reforms helped stabilize Social Security for decades. Today’s challenge comes with less time, higher debt, and deeper political division.

Why Pressure Is Growing

Several forces are weakening Social Security’s finances at once. The ratio of workers to beneficiaries is shrinking. Americans are having fewer children, with the U.S. fertility rate at a record low. Meanwhile, lower net migration means fewer workers are paying into the system.

Recent tax changes may also reduce trust fund revenue by lowering the amount of taxes paid on Social Security benefits. That could deepen the shortfall and leave lawmakers less time to make gradual changes. Inflation has made the problem feel more immediate for retirees. Cost-of-living adjustments help, but often lag the real costs seniors face, especially medical care and housing.

Congress Has Options

Decades of congressional inaction have narrowed the range of workable solutions. The window for gradual, manageable reform is closing fast.

Lawmakers have a familiar set of options available. Raising the payroll tax rate or lifting the earnings cap subject to payroll tax would bring in more revenue. Adjusting the benefit formula for higher earners or gradually raising the full retirement age would slow benefit growth.

The Trustees emphasized that acting sooner allows changes to be spread across more generations, reducing the burden on any single group. Congressional action remains uncertain, making personal preparation essential regardless of what lawmakers ultimately decide.

How to Prepare Now

Start by reviewing your claiming strategy. Social Security can be claimed as early as age 62, but monthly benefits rise when you delay. Waiting until age 70 can increase monthly benefits by up to 24 percent compared with full retirement age.4

Next, reduce your dependence on one income source. Part-time work, consulting, rental income, or savings can help bridge the gap if benefits are reduced. A plan with several income streams is stronger than one built around one government check.

Maximizing retirement accounts can also help. Workers over 50 may be able to use catch-up contributions in 401(k)s and IRAs. Extra savings today can help replace part of a possible Social Security cut later.

Healthcare planning deserves special attention. Medical costs can rise faster than headline inflation, and a smaller Social Security check could make them harder to absorb. Supplemental insurance, long-term care planning, and emergency savings can help protect retirement income.

Gold and Purchasing Power

Physical gold can play an important role in preparing for Social Security uncertainty. Benefit checks are paid in dollars, and inflation can weaken what those dollars buy. Gold is a hard asset with a long history of preserving purchasing power during periods of inflation, currency weakness, and financial stress. It can also respond to economic pressure more quickly than annual COLA adjustments.

Unlike Social Security benefits, gold does not depend on a vote in Congress. For retirees concerned about reduced benefits and rising costs, physical precious metals can add protection outside the traditional dollar-based system.

Conclusion

Social Security will likely remain a major part of American retirement. But the Social Security funding crisis is, as Michael Peterson of the Peter G. Peterson Foundation stated, “both highly predictable and fully avoidable.” The solutions are well understood. What has been missing is urgency. Individuals who begin building more resilient retirement income plans now will be far better positioned regardless of how Congress ultimately acts.5

If you want to protect your portfolio with physical precious metals in a Gold IRA, contact AHG today at 800-462-0071.