- Gold continues to behave like a high-quality liquid asset, even without official recognition.

- Institutional demand and potential reclassification could drive stronger demand and higher prices.

- Physical gold can help protect your finances with both liquidity and long-term stability.

Liquidity When It Matters Most

When markets come under pressure, liquidity disappears fast. Buyers step back, spreads widen, and assets become difficult to move. Gold has often behaved differently, continuing to trade smoothly during stress.

Now, major players in the gold market are pushing to make that role official. The World Gold Council and London Bullion Market Association are working to have gold officially recognized as an asset banks can quickly convert into cash when fiscal pressure hits. Their case is built on how gold supports stability in the global financial system. For individual investors, that same set of qualities can play a very different role, helping protect access to value when conditions shift.1

What Banks Need in a Crisis

To understand why this matters, consider how banks prepare for stress. After the 2008 financial crisis, regulators introduced rules requiring banks to hold assets they could quickly convert into cash during stress. These assets are expected to be stable, widely accepted, and easy to sell even when markets are under pressure.

These assets are known as High Quality Liquid Assets, or HQLAs. They are designed to help banks meet short-term liquidity needs during periods of stress, including a 30-day window of potential outflows, a requirement often referred to as the Liquidity Coverage Ratio.

Cash and U.S. Treasuries sit at the top of that list. They are trusted, liquid, and deeply embedded in the global financial system. Gold is not officially included in that same category for liquidity requirements, but it shares many of the same characteristics.2

Gold Already Fits the Profile

Regulators define these assets by core characteristics. They are expected to carry low risk, be easy to value, trade in large markets, and maintain liquidity during stress. Gold aligns with each of these traits.

Gold trades in a global market that operates across time zones, with consistent demand from central banks, institutions, and private investors. Activity does not rely on a single exchange or a narrow group of buyers. When volatility rises, participation tends to increase rather than fade.

Liquidity is only part of the story. Gold has also shown a pattern of holding its value during periods when risk assets come under pressure. In market downturns, investors often shift toward assets they believe can preserve purchasing power. Gold has historically been one of those destinations. Not because of short-term price moves, but because it is not tied to the performance of a company, a currency, or a government balance sheet.

No Counterparty, No Dependency

Stocks depend on earnings. Bonds depend on issuers. Currencies depend on monetary policy. Gold stands apart from all three. It does not carry counterparty risk, and it does not rely on a promise to pay.

Recent years have provided clear examples. During the 2023 banking crisis, liquidity tightened across several parts of the financial system. Some assets became difficult to price and even harder to sell without taking losses. Gold continued to trade, rising more than 8% within a month. It provided a source of stability when liquidity mattered most.3

Despite this, gold is not currently included in bank liquidity buffers, even though it carries a 0% risk weight under capital rules. Under longer-term funding standards, it is often treated more like a commodity, which limits its formal role despite its real-world behavior.

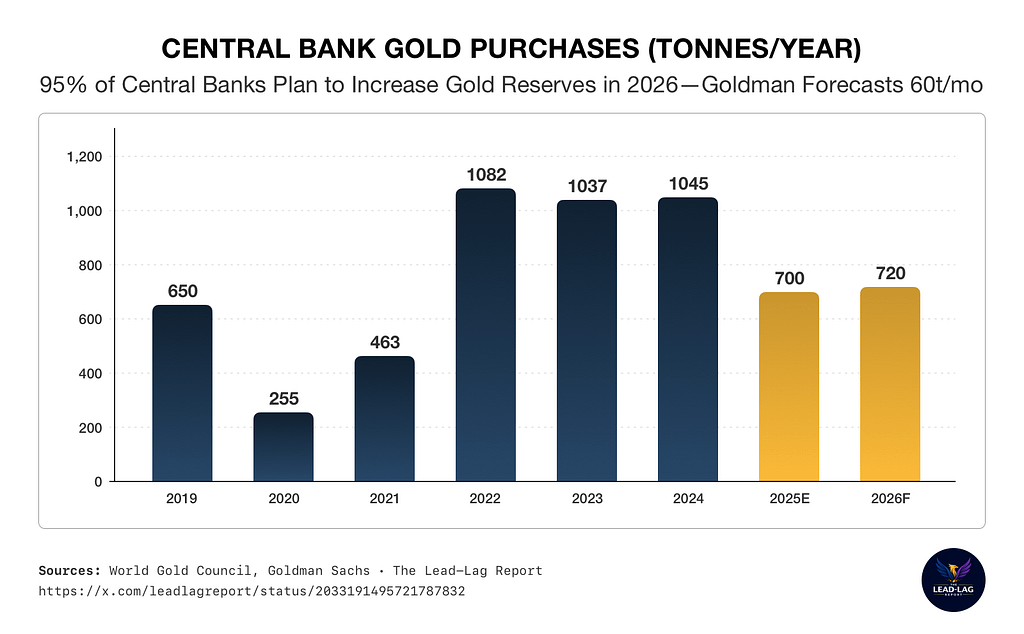

Why Central Banks Are Buying

4

Central banks clearly recognize gold’s dual role. After several years of record buying, they continue adding to their reserves at levels well above historical averages. This sustained demand reflects a broader shift toward assets that operate outside traditional financial systems. Their consistent demand adds another layer to gold’s role, reinforcing its position as both a long-term store of value and a liquid asset.

What This Means for You

Markets do not always move in a straight line and liquidity can matter as much as returns. Assets that seem dependable during calm periods can behave very differently under pressure.

Gold has remained accessible across a wide range of environments. It trades globally and does not rely on a financial intermediary to hold its value. Many investors use gold to help balance a broader portfolio, particularly during uncertain periods.

The Bigger Shift Taking Shape

The discussion around High Quality Liquid Asset status highlights something important. Gold may not carry that formal label today, but its behavior continues to align with the qualities regulators look for. Stability, liquidity, and independence are not theoretical. They have been demonstrated in real market conditions.

Some analysts believe that if gold is formally recognized in this way, it could increase central bank demand, tightening supply and putting additional upward pressure on prices.5

Conclusion

For those looking to diversify and protect long-term savings, physical gold remains a consideration. Whether held directly or within a Gold IRA, it offers a way to own a tangible asset not tied to traditional financial markets.

Economic conditions change. The need for stability and liquidity does not. To learn more about protecting your funds with precious metals, call American Hartford Gold today at 800-462-0071.