- Private credit carries hidden leverage, unclear valuations, and liquidity risks similar to those seen before the 2008 crisis.

- Rising losses and withdrawal limits suggest stress may already be building beneath the surface.

- Precious metals in a Gold IRA can help protect your finances since they are independent of the traditional credit system.

Private Credit Risks Are Building

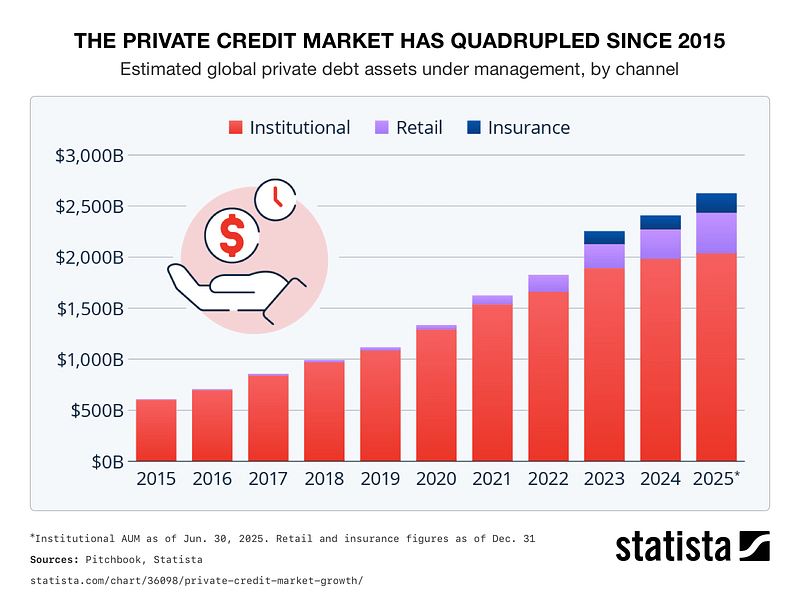

A story is unfolding in the private credit market that most Americans have never heard of, and that’s a problem. While headlines chase the stock market’s daily swings, a $3.5 trillion lending industry has quietly built up many of the same structural weaknesses that made the 2008 financial crisis so devastating. With the risk of a systemic crisis building, more people are considering safe-haven assets that are independent of the traditional financial system.

What Private Credit Actually Is

Private credit is direct lending by non-bank funds to companies that skip traditional banks and public markets. Stricter rules after 2008 made banks less willing to hold this kind of risk. Private equity firms like Blackstone and Apollo stepped into the gap, raising massive pools of investor money to lend to mid-sized companies. The pitch centered on steady income and attractive yields. For years, funds grew fast enough to pay departing investors with new investor cash, without ever selling a loan to raise money.

2008 Comparisons

The 2008 financial crisis became dangerous when hidden debt, unclear risks, and fragile funding systems all broke down at once. Private credit is showing similar warning signs, including hard-to-sell loans, valuations set by fund managers instead of public markets, and limited transparency about where the greatest risks may be hiding.

The Stress Is Already Showing Up

An analysis of 53 publicly traded business development companies, or BDCs, found that 28 lost money in the first quarter of 2026. Only 12 reported losses a year earlier, while 10 did so in 2024.

The group moved from an average profit of $26 million in the first quarter of 2025 to an average loss of $7.6 million one year later. Loan markdowns were a major factor, with software borrowers disrupted by artificial intelligence creating particular concern.

Several major funds have also reported significant losses. Blue Owl’s OTF fund recorded its largest markdown since launch. FS KKR posted its second-largest realized loss, while Crescent Capital BDC reported its highest quarterly losses since 2020.2

Leverage Hiding in Plain Sight

Part of what makes this risk hard to see is how it’s being financed. Average borrowing costs at listed BDCs has climbed roughly 20% over the past two years. At the same time, funds are relying more heavily on payment-in-kind financing, known as PIK. With PIK, borrowers pay interest by adding it to existing debt instead of cash. PIK income represented 8.1% of BDC interest and dividend income in 2025, about twice its pre-2020 level. PIK can make reported income appear stronger without producing cash. Industry professionals describe rising PIK income as a possible sign of weakening credit quality.3

Add to that a growing reliance on off-balance-sheet borrowing. These joint ventures and special-purpose vehicles don’t appear in standard leverage calculations. Among the few funds that disclosed complete data, total borrowing jumped 80% in a single year once these hidden structures were added back in. 4

Withdrawal Limits Reveal the Liquidity Problem

BlackRock’s $26 billion HPS Corporate Lending Fund offers a clear example. During the first quarter of 2026, fund holders requested withdrawals equal to 9.3% of shares. BlackRock limited withdrawals to the fund’s 5% quarterly cap. Requests climbed to roughly 13% during the second quarter, and the fund imposed the limit again.5

The private credit liquidity mismatch is playing out in real time. These funds were marketed to retail investors with the promise of periodic access to cash. But the underlying loans can’t be sold quickly without taking a loss. So, when enough investors want out at once, the fund simply refuses.

In a sign that private credit managers may be bracing for trouble, lending volume has fallen more than 50% even as fundraising has jumped more than tenfold.

Regulators Are Worried

European regulators are pressing U.S. officials for information about private credit funds. They are openly worrying about hidden risks that could spread through banks, insurers, and pension funds. If regulators cannot see where the money and risk are hiding, individual investors have little chance of knowing either.

Conclusion

Before the 2008 financial crisis, everything appeared stable. In hindsight, the warning signs were everywhere: hidden leverage, complicated financing, and institutions tied together by risks few people understood. Once the cracks appeared, the damage spread quickly and nearly brought down the entire financial system.

Private credit shows the same warning signs today. No one can predict whether private credit will trigger another crisis, but history shows the danger of waiting until the problems become impossible to ignore. Especially now that there is a push to allow retirement funds to invest in private credit companies.

Physical gold offers a way to hold value outside the credit system. Its value does not depend on a borrower, fund manager, or Wall Street institution.

Learn how to protect your savings with a Gold IRA by calling American Hartford Gold today at 800-462-0071.