The AI Market Bubble

Almost 100 years after the Great Crash of 1929, the economy once again sits atop a shaky summit. Financial journalist Andrew Ross Sorkin draws striking parallels between the exuberance of the 1920s and the speculative energy of today’s markets. Just as stocks soared to record highs a century ago before the devastating collapse, today’s rally shows familiar signs of overextension. His warning is clear: a downturn is inevitable.

“I just can’t tell you when, and I can’t tell you how deep,” Sorkin said. “But I can assure you, unfortunately, I wish I wasn’t saying this, we will have a crash.”1

Today’s economic landscape looks far different from the Jazz Age. But the underlying dynamics of investor optimism, speculation, and concentrated market power are disturbingly similar. The 1920s ended with panic and widespread financial ruin. Could today’s AI-driven rally face a similar fate?

Voices of Caution

Several business leaders are expressing concern about the scale and sustainability of AI spending. Goldman Sachs CEO David Solomon remarked that much of the capital being deployed “doesn’t deliver returns.” Jeff Bezos described the current environment as “kind of an industrial bubble.” OpenAI CEO Sam Altman cautioned that “people will overinvest and lose money” in this phase of AI growth.2

More than 150 executives, investors, and founders echoed those concerns at a recent Yale CEO Summit. Reports show that AI-related capital expenditures have overtaken the U.S. consumer as the main engine of growth in early 2025. JP Morgan Asset Management noted that AI-linked companies have contributed roughly 75% of S&P 500 returns, 80% of earnings growth, and 90% of capital spending growth since late 2022.3

Morgan Stanley Wealth Management estimates that “hyperscaler” companies, those powering AI infrastructure, now spend about $400 billion annually on capital expenditures. This spending alone is adding around one percentage point to GDP growth. Even as consumer spending slows. The scale underscores how dependent markets have become on a narrow slice of the economy.

A Rally Built on Concentration

RBC’s Kelly Bogdanova points out that after two years of record earnings, growth among the “Magnificent Seven” technology firms is expected to align more closely with the broader market in 2026. Yet, the gap between the tech sector’s share of market capitalization and its share of profits has widened dramatically.4

Since October 2022, when the bear market bottomed, the S&P 500 has risen 90%. Most of those gains have come from a handful of companies; Nvidia, Microsoft, and others tied to AI data-center infrastructure. The remaining 493 stocks in the index are up only about 25%. This extreme concentration makes the rally vulnerable to even small disruptions in AI spending or sentiment.5

A recent MIT study found that 95% of 52 organizations surveyed saw zero return on investment after collectively spending $30 to $40 billion on generative AI initiatives. That imbalance between investment and payoff is prompting more analysts to question how long the AI surge can continue.

The Risk of a “Cisco Moment”

Morgan Stanley’s Lisa Shalett describes the current boom as a “one-note narrative” powered by relentless capital expenditures in AI. She worries about a “Cisco moment”. A reference to the dot-com era company whose stock plunged 80% when the bubble burst in 2000. Shalett doesn’t expect a collapse in the next nine months. But she warns it could come within two years. “We’re a lot closer to the seventh inning than the first or second inning,” she said.6

Even former dot-com executives see the similarities. Cisco’s longtime CEO John Chambers said that the optimism surrounding AI reminds him of “irrational exuberance on a really large scale.” He predicts a “future bubble for certain companies” that fail to turn their massive investments into sustainable revenue.7

A Self-Contained Financial Loop

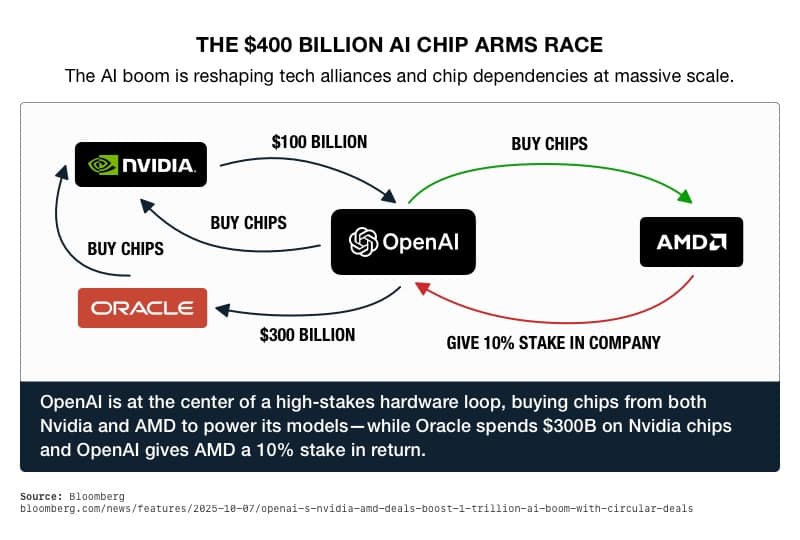

Perhaps the most striking example of risk lies in the circular nature of AI financing. Nvidia is the most valuable company in history with a market cap exceeding $4.5 trillion. They are involved in nearly every major deal. In September, Nvidia invested $100 billion in OpenAI and another $5 billion in Intel. OpenAI, in turn, is taking a 10% stake in AMD. Microsoft, a major OpenAI shareholder, is also a major Nvidia customer. And Nvidia holds equity in CoreWeave, a company that supplies cloud computing services to Microsoft.8

This tight web of mutual investment has raised alarms about a potential “self-contained loop” of money recycling through the same entities. Shalett calls it a sign that the market may be entering its final innings. When too much value depends on interconnected players, one stumble can cascade through the system.

How a Bubble Could Burst

Analysts see three main pathways for a potential AI-driven correction:

- Concentration leads to contagion: If just one or two dominant players falter, their interconnected relationships could trigger a chain reaction across global markets.

- Governance conflicts expose weaknesses: AI companies operate with minimal oversight, much like crypto exchanges before 2022. Any major failure or misuse could prompt panic and regulatory crackdowns.

- Disruptive innovation makes current investments obsolete: Advances in chip design or quantum computing could render today’s massive data-center investments unprofitable for years.

Conclusion

The optimism driving markets today is reminiscent of the exuberance that preceded 1929 and 2000. Whether the AI surge proves transformative or transient, Sorkin’s warning stands: no rally lasts forever.

For retirement fund holders, that means diversification and prudence remain essential. History shows that even in times of innovation and prosperity, market manias can turn quickly. As the U.S. enters what some call a “new roaring 20s,” remembering the lessons of the old one may be the surest way to preserve wealth. To learn more about how you can protect your savings with a Gold IRA, call us today at 800-462-0071.