- Panda bonds allow foreign borrowers to raise money in yuan instead of dollars.

- Brazil’s planned record panda bond sale is another sign of incremental de-dollarization.

- Physical gold can help protect your finances as de-dollarization threatens the dollar’s purchasing power.

China’s Dollar Challenge Grows

Brazil is preparing to sell $735 million in yuan-denominated bonds inside China’s own domestic market. The deal would mark the largest first-time sovereign panda bond sale on record. Brazil ranks as one of the world’s largest economies, a G20 member and a major BRICS power.1

When an economy as large as Brazil starts borrowing in yuan, the message gets louder: the dollar’s grip on global finance is starting to crack.

What Panda Bonds Actually Are

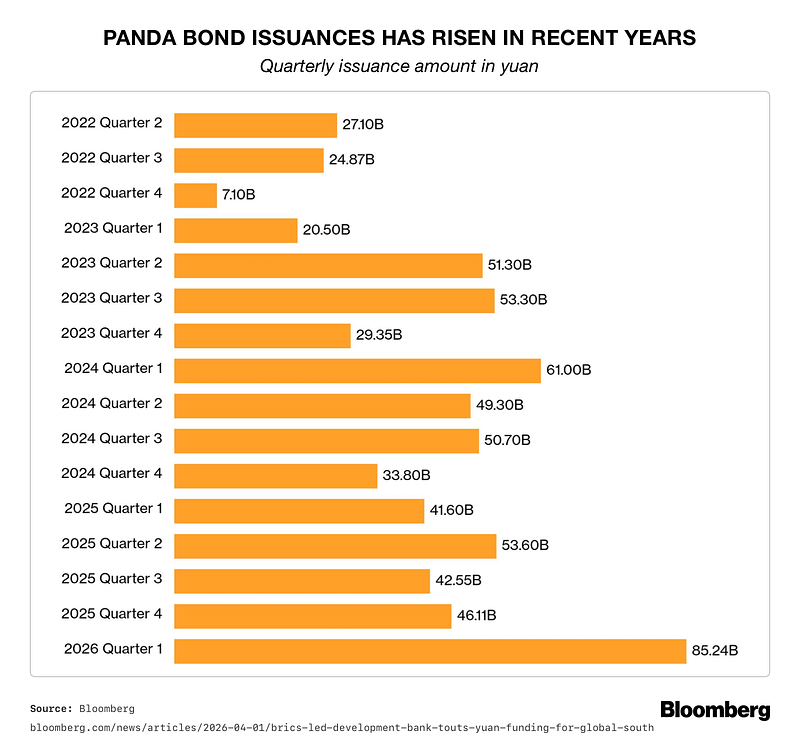

Panda bonds are yuan-denominated debt sold by foreign governments, banks, and corporations inside China’s own bond market. Foreign issuers borrow directly in yuan rather than dollars, often at rates far below what they could get at home. Pakistan recently issued yuan bonds at 2.5% interest, compared to an 11.5% benchmark domestically.

The numbers show how fast this market is growing. Issuance hit roughly 133 billion yuan by late May of this year, nearly double the pace from the same period last year. Foreign issuers now account for 41% of the market, up from just 27% in 2023. Sovereign borrowers keep lining up: Pakistan, Kazakhstan, Slovenia, the UAE, and now Brazil.2

Why This Speeds Up De-Dollarization

Every new sovereign that borrows in yuan adds legitimacy to the currency as a global funding tool. The New Development Bank, the multilateral lender founded by BRICS nations, has openly pitched China’s onshore bond market as one of the cheapest sources of financing anywhere in the world.

According to the bank’s director of treasury, Zhongxia Jin, the yuan is becoming not just an alternative to the dollar, but a “key pillar of the global financial architecture.”4

The bank also pushed maturities out to 10 years for the first time. Short-term borrowing can be temporary. A 10-year structure shows a durable commitment.

Countries that borrow in yuan reduce their exposure to US interest rate policy. They also step outside the reach of dollar-based sanctions. For nations aligned with China or BRICS, that independence carries real strategic value alongside the cost savings.

The scale remains modest compared to the multi-trillion-dollar dollar system. Still, the direction of travel matters more than the current size. Every additional issuer normalizes a world where the dollar is one option among several major reserve currencies.

What It Means for the US Economy and Retirees

The United States has long enjoyed what economists call an exorbitant privilege: the ability to borrow cheaply because the rest of the world wants dollars. Foreign governments buying Treasuries has helped keep US interest rates lower than they would otherwise be.

As more global savings flow into yuan-denominated assets instead of Treasuries, that advantage begins to erode. Reduced foreign demand for US debt can put upward pressure on interest rates and inflation over time. A weaker dollar buys less abroad and can push up the cost of imported goods at home.

Retirees carry a disproportionate share of this risk. Fixed incomes do not stretch as far when inflation rises. Bond-heavy portfolios lose value in real terms when the currency backing them weakens. Savings built up over decades can quietly lose purchasing power even while the account balance stays the same on paper.

A Slow Shift with Real Consequences

De-dollarization is not a single event. It builds through years of small decisions, like Brazil’s bond sale or Pakistan’s cheaper borrowing terms. Each one chips away at the assumption that the dollar will always be the default currency of global finance.

Uncertainty about the dollar’s long-term value is not an abstract policy debate. It is a direct threat to how far a retirement account will stretch ten or twenty years from now. Currency risk rarely announces itself loudly. It shows up gradually, in higher prices and a shrinking real value of savings.

Conclusion

Physical gold has served as a store of value for thousands of years precisely because it sits outside any single government’s monetary policy. It cannot be printed, devalued by a central bank, or defaulted on the way currency-denominated debt can be. As the dollar’s global dominance faces new pressure from trends like the rise of panda bonds, gold offers a way to hold wealth that does not depend on any one nation’s fiscal choices.

Retirees have used gold to anchor a portion of their savings against currency depreciation and inflation. A Gold IRA allows that protection to sit inside a tax-advantaged retirement account, combining the stability of physical precious metals with the structure of traditional retirement planning.

If you want to protect your portfolio with physical precious metals in a Gold IRA, contact AHG today at 800-462-0071.