- Moody’s and Fitch Ratings downgraded the credit rating of the banking industry

- The downgrade was due to high interest rates and growing risk of bank failures

- Experts turn to physical precious metals as banks and the government become worse stores of wealth

Banking Industry Downgraded

The phrase “like money in the bank” is taking on a new meaning nowadays. The once secure banking industry is growing increasingly riskier. Bank stability is being challenged with high interest rates, rising deposit rates and slumping profitability. Now they can add a rating downgrade to their list of troubles. On the heels of a US credit downgrade, a depreciating financial industry threatens to undermine the broader economy.

Last week, Moody’s Investment Services downgraded the credit rating of 10 mid-sized banks by a single notch. They cited growing financial risks and strains that could erode their profitability. They also warned of a review of six other lenders and assigned a negative outlook to 11 other banks.

Moody’s actions come after a banking crisis that started in March with the sudden collapse of Silicon Valley Bank. Once the nation’s 16th largest bank, their depositors grew fearful of the bank’s solvency and made a classic bank run. Signature Bank and First Republic Bank soon followed, leading to more concerns about the banking industry’s stability.

Moody’s downgrade is on the heels of one from Fitch Ratings. In June, Fitch lowered the banking industry to AA- from AA. Fitch Ratings is now warning the banking industry could be downgraded again from AA- to A+. If that happens, Fitch would be forced to reevaluate ratings on each of the more than 70 banks it covers. Shares of JPMorgan, Bank of America and Citigroup fell on news of the warning.

Downgrade Meaning

Banks rely on bond sales to help fund their operations. A downgrade makes those issuances more expensive. That’s because Investors demand more return to own lower rated bonds. As a result, costs increase for banks and profits go down.

Impact of Fitch Downgrade

Another Fitch downgrade creates a new problem for banks. If the industry’s score is downgraded to A+, then it would be lower than some of its top-rated lenders. The country’s two largest banks by assets, JPMorgan and Bank of America, would likely be cut to A+ from AA-. This is because banks can’t be rated higher than the environment in which they operate. Which in turn triggers downward adjustments for their smaller rivals. Weaker lenders would be moved closer to non-investment grade status.

Tough Timing

Regulators want banks to issue more bonds as they become more expensive for the banks. The FDIC, Federal Reserve and Office of Comptroller of the Currency are trying to stop the long simmering banking crisis from boiling over. They want to prevent any future bank runs. Regulators want the banks to issue more long-term debt to stabilize them. The long-term debt is meant to absorb losses if the bank fails. It is meant to make it easier for banks to hold onto depositors and slow down a run.

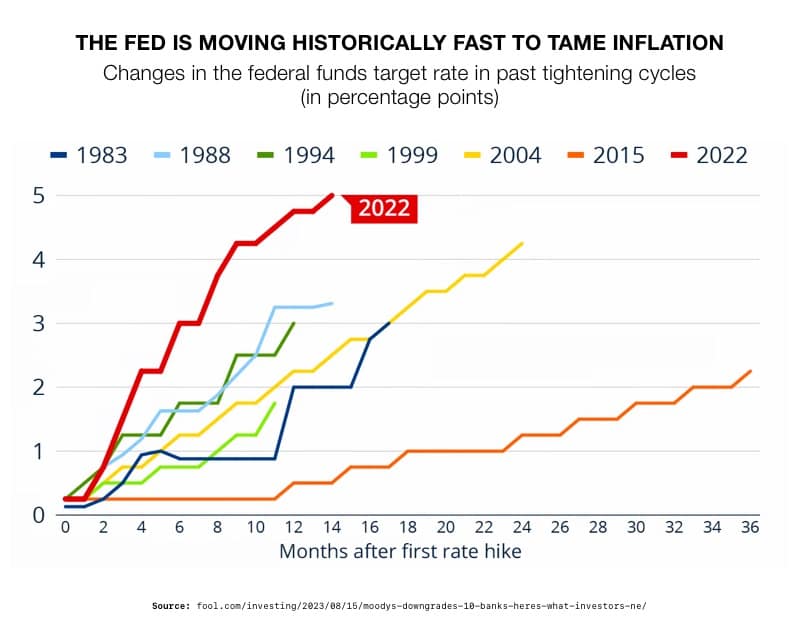

Role of Interest Rates

The Federal Reserve rapidly raised interest rate to fight inflation. Rates went from almost zero to 5.5% within a year.

1

1

Minneapolis Federal Reserve President said the risk is that if inflation is not completely under control, the Fed may have to raise rates further. Banks “might face more losses than they currently face today.” According to CME Group’s FedWatch Tool, market participants believe the Fed will hold interest rates near their current levels well into the first half of next year. They want to bring inflation down to the central bank’s 2% target.2

Prolonged higher interest rates could force Fitch to go through with the downgrade. Record high rates put extreme downward pressure on the industry’s profit margin. In addition, higher rates lead to more defaults. The more defaults, the more likely the downgrade is going to happen.

The collapse of the commercial real estate market is also threatening small and mid-size banks. They are the primary lenders in that industry. Small banks hold 67% of all commercial real estate loans. Developers typically only paid the interest on real estate loans. They would refinance when the principle came due. But high interest rates are making that unaffordable. As a result, there is an exponential increase in defaults. These nonpayments are hammering the bottom line of small banks. 3

Follows US Downgrade

Earlier this month, Fitch Ratings downgraded the credit rating of the United States from “AAA” to “AA+.” Fitch cited the nation’s growing debt and continued partisan standoffs over the debt limit. Fitch Ratings said these political standoffs have prompted spiraling national debt and a lack of confidence in the US government to manage it.

Moody’s and Fitch are exposing an unwelcome truth about the banking industry and the United States government. They are both becoming more unstable. Once solid secure repositories for investors, both banks and the US are becoming riskier and riskier investments. For those who are interested in securing their retirement funds, safe haven assets like precious metals offer a safer alternative. A Gold IRA from American Hartford Gold can preserve your wealth as the bedrock of the US (and world) financial system cracks. Contact us today at 800-462-0071 for a personalized gold solution.