- New York Community Bancorp shares plummeted due to devalued assets and tighter regulations

- The sinking regional bank sparked fears of a sector wide banking crisis

- A Gold IRA can insulate portfolios from the impact of a collapsing banking system

Banking Crisis Blowing Back Up

It has been one year since the banking crisis resulted in the second and third largest bank collapses in US history. And now a new troubled regional lender, New York Community Bancorp (NYCB) is stoking fears that the simmering banking crisis is about to reignite.

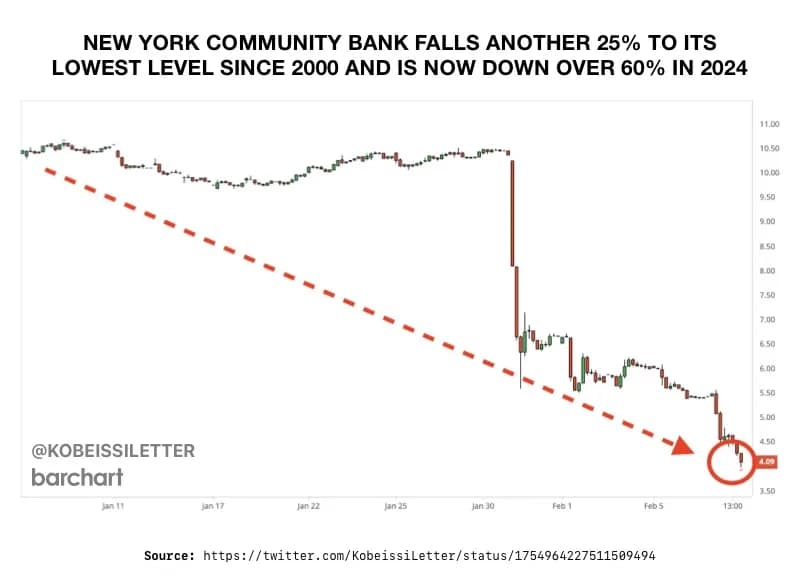

New York Community Bancorp stock plummeted after releasing a terrible earnings report. The report showed massive, unexpected losses on commercial real estate loans. The bank revealed a fourth quarter loss of $252 million instead of a third quarter gain of $207 million. In response, the bank slashed its dividend by 70% and was forced to stash a half billion in cash away to protect against future losses, plus $185 million in net charge-offs. Their shares have lost almost half their value in a week, dropping 44.6%.1

2

2

Even worse, this came as a shock because the bank had not prepared markets for the bad news. Moody’s has since put its ratings of NYCB under review. The bank shares can now be downgraded into “junk” territory.

The fall of NYBC ties directly back to the earlier stage in the banking crisis. NYBC ballooned in size last year after taking over the assets of the fallen Signature Valley Bank. Not only did NYCB trap themselves with the flailing SVB assets, but the acquisition also pushed them above the $100 billion asset mark. That forced them into tighter government standards that were imposed to prevent another round of regional bank collapses. NYBC had to devote more funds to make sure they could stay liquid in case of a crisis.

Fear of the Crisis Spreading

Fears of contagion amongst regional banks grew. Regional banks are overleveraged with loans to a desperately struggling commercial real estate sector. The average regional bank stock has lost 10% over the past week.

Other banks are drawing scrutiny. M&T bank has similar size and assets as NYBC. Big banks have been bracing against real estate losses by setting money aside for months. Overseas banks are not insulated from the panic. Azora Bank of Japan saw shares drop 20% due to its portfolio of US office loans. It could have fallen further if there wasn’t a maximum drop allowed on the Japanese market. Deutsche Bank had to increase its loss provisions for its US commercial loans nearly fivefold.

Fed Chair Jerome Powell described the situation as a “sizable problem.” The rapid increase in interest rates is what doomed Signature Valley Bank. High rates combined with low valuations to put commercial real estate holdings underwater. But there was a secondary effect. Banks had to raise interest rates to compete with the government for depositors. This eroded their net interest income – the difference between what lenders earn on loans and pay on deposits.3

The Federal Reserve put a lid on the earlier phase of the banking crisis by printing money and throwing it at the banks. Their “Bank Term Funding Program” with $25 billion in new money paused the crisis without solving the underlying problems.

Bank Runs

Last year’s banking crisis was made worse as fears of a bank run grew. Customers withdrew $42 billion in a single day from Silicon Valley Bank. It was left with $1 billion in negative cash balance. The staggering withdrawals unfolded at a speed enabled by digital banking and were likely fueled in part by viral panic spreading on social media platforms and, reportedly, in private chat groups.4

Regulators say a run is unlikely. But it is not impossible. Like they say, a flood always begins with a single drop of rain. With banks required to only keep a small fraction of customer deposits on hand, another run could be disastrous.

And with $1.5 trillion of commercial real estate loans hovering near default, there is reason to believe a nationwide banking crisis could flare up to epic proportions. A new report from the National Bureau of Economic Research indicates that nearly half of all banks now risk default. Even a 10% default rate would cost commercial banks $80 billion.5

The floodwaters could break as soon as March 11. On that date, the Fed’s emergency bank funding program will shut down for good. Without a government bailout waiting in the wings, the country may be stricken by a full-blown banking crisis that affects every sector of the economy and sinks the stock market.

The government recognizes the danger even if they aren’t prepared to handle it. The Financial Stability Oversight Council, of which Treasury Secretary Janet Yellen, Federal Reserve Chair Jerome Powell and US Securities and Exchange Commission Chair Gary Gensler are members, released a report last December that cited commercial real estate as a major potential financial risk.

“As losses from a [commercial real estate] loan portfolio accumulate, they can spill over into the broader financial system,” they wrote. “Sales of financially distressed properties can reduce market values of nearby properties, lead to a broader downward CRE valuation spiral, and even reduce municipalities’ property tax revenues.”6

Conclusion

The only people profiting from the failing banks are the short sellers who made over $685 million in paper profits. And that is on top of hedge funds clearing unrealized profits of $7.25 billion after the March 2023 bank failures.7 If you aren’t in that elite club of investors, then you need to take precautions to protect the value of your portfolio. With no counterparty risk, a Gold IRA from American Hartford Gold can insulate your portfolio from a collapsing banking system. Contact us today at 800-462-0071 to learn more.