Retirement in Uncertain Times

Many Americans thought they were doing everything right. They saved in their 401(k). They paid off their mortgage or built equity in their homes. They followed the plan. But now, that plan feels shaky.

A wave of layoffs is hitting those over 50 as new hiring slows. High mortgage rates and low supply are leaving homeowners “house rich and cash poor”. The stock market looks strong on paper but is held up by a small group of AI stocks that could easily stumble and punish 401(k)s. Meanwhile, inflation keeps eating into savings, and debt keeps growing.

All of which are limiting contributions or forcing withdrawals. Which begs the question: how ready are Americans for retirement?

The Shrinking Nest Egg

The old “4% rule” says you can withdraw 4% of your nest egg each year and be safe. But that math falls apart fast. A $250,000 account gives you just $10,000 your first year. Add the average $24,000 in Social Security, and that’s $34,000 total. For most people, that barely covers essentials.

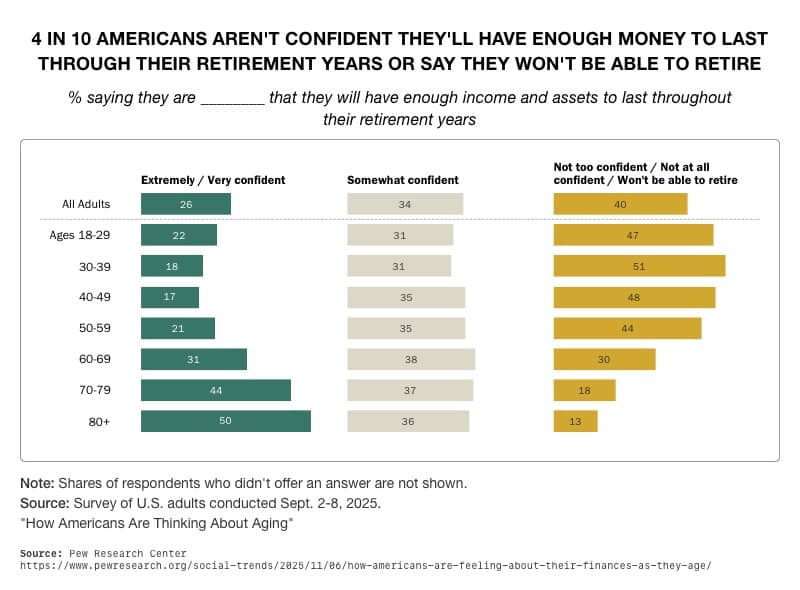

Goldman Sachs Asset Management says 58% of workers believe their savings won’t last thru retirement. That fear of running out of money is growing, and for good reason. Inflation and higher living costs are hitting everyone. Even households with solid incomes are often stretched thin, living paycheck to paycheck. They are weighed down by debt, lifestyle and healthcare costs. These expenses have forced many workers to dip into or pause their retirement savings. 1

2

Greg Wilson is head of retirement at Goldman Sachs Asset Management. He stressed that simply saving more may not be enough. He said many people will need more thoughtful investment and retirement income strategies to close their savings gap.3

A National Savings Shortfall

Other sources echo similar concerns. Data shared by Dave Ramsey found that 42% of Americans are not saving for retirement at all. Only about half have calculated how much they will need. Vanguard’s national analysis showed that three in five Americans are not on track to meet their retirement spending needs. The rest face an estimated $5,000 annual shortfall.4

For many, that means they may need to work longer, scale back spending, or find other income sources. The Motley Fool reported that 47% of working households risk falling short, with over half having less than $100,000 saved. One in three has less than $25,000. These statistics show how fragile America’s retirement situation is. 5

Retirement Crisis Becomes National Threat

The consequences go beyond the personal. When half the country can’t afford to retire, the entire nation feels the strain. As more seniors struggle to meet basic needs, demand for Social Security, Medicare, and other safety nets will surge. The government will be forced to spend more at a time when astronomical debt is already consuming its budget.

That pressure could lead to higher taxes, more borrowing, and painful cuts to health, defense, and infrastructure. Rising interest payments and ongoing deficits would only tighten the squeeze. Leaving fewer options to respond to future crises. Over time, this imbalance could weaken growth, increase inequality, and erode public trust. What starts as an individual retirement crisis could quickly become a national one.

Building a More Secure Future

The numbers paint a difficult picture. But the good news is that individuals can still strengthen their retirement outlook. Start by making full use of your employer plan and matching contributions. Combine scattered retirement accounts so you can track your progress. If possible, delay taking Social Security to boost your monthly income later. That can increase payments by about 8% per year for each year benefits are delayed beyond full retirement age.6

But the key is to prepare wisely, not just save. A diversified approach that includes tangible assets can give your portfolio strength when markets fall.

Gold’s Role in a Stronger Retirement Plan

Physical gold remains one of the most reliable ways to protect long-term wealth. It holds value through inflation, market downturns, and economic uncertainty. Unlike paper assets, gold is real and in your control.

Including even a small percentage of physical gold in your retirement portfolio can help balance risk. Gold often moves separately from stocks and bonds, offering stability when markets swing. Through a Gold IRA, investors can hold physical gold with the same tax advantages as traditional retirement accounts.

Gold is also liquid, meaning it can be converted to cash when needed. It’s a hedge, a store of value, and a safeguard against the unexpected.

Conclusion

There is a growing retirement readiness gap across income levels and age groups. Inflation, debt, and market concentration have created new challenges that traditional savings strategies may not fully solve.

A diversified approach that includes physical gold can provide a more stable foundation for the years ahead. In a time when too many Americans are uncertain about their retirement future, holding tangible wealth can offer lasting peace of mind. Contact American Hartford Gold today at 800-462-0071 to learn how physical precious metals can benefit you.