- The U.S. faces a $40 trillion debt and a massive refinancing challenge.

- Rising interest costs and volatility threaten the economy and retirement savings.

- Protect your finances by holding physical precious metals in a Gold IRA.

Debt Dangers Continue to Mount

The U.S. economy is in a pressure cooker.

Decades of borrowing have built up $37 trillion in national debt, and that figure is projected to hit $40 trillion within the next year. For now, the lid is still on, but heat is building fast. And when it erupts, the damage to the economy, and your retirement savings, will be severe.1

In 2025, nearly a third of the national debt will come due, creating a massive refinancing problem. According to the Treasury’s Office of Debt Management, as of April 2025, about 31.4% of the outstanding national debt, roughly $11 trillion, needed to be refinanced within the next 12 months alone.2

When including the debt that matures in 2026, the total refinancing obligation for these two years approaches $18 trillion. This means the Treasury will need to roll over trillions in bonds. All at today’s much higher interest rates.

This isn’t just a line in a government ledger. When debt piles up and interest rates rise, the cost of keeping the lights on in Washington skyrockets. In 2024, interest payments on the national debt surged 34% to $949 billion, more than we spent on the military and Medicare. And that was before the heaviest wave of refinancing even began. Hence, President Trump’s urgency to have the Fed lower interest rates.3

The Refinancing Wall Ahead

During 2020 and 2021, the government refinanced its debt at rock-bottom rates, locking in cheap payments. Now, the bill is coming due…with interest. Lots of interest.

In 2025 alone, $9.2 trillion in debt must be refinanced. About 70% of it hit in the first half of this year. Another $9.3 trillion will need refinancing between April 2025 and the end of 2026.

Michael Howell is founder and CEO of Crossborder Capital. He noted that global liquidity, which is the availability of cash and credit in financial markets, is currently at its highest level since COVID. But it is set to peak by early 2026. After that, the massive debt refinancing could trigger a severe liquidity crunch. And send volatility soaring. Howell fears the turmoil may end suddenly, much like the 1987 market crash.4

If Treasury yields spike to attract buyers, borrowing costs ripple through the economy. Raising rates on mortgages, business loans, and credit cards. For retirees and savers, this can mean falling asset values, lower returns, and higher risks in once “safe” investments.

Washington Raises the Ceiling

As the Treasury braces for this massive refinancing challenge, lawmakers in Washington made another high-stakes move. They raised the debt ceiling by $5 trillion with the passage of President Trump’s “One Big Beautiful Bill Act” in July 2025.5

The increase, from $36.1 trillion to $41.1 trillion, is the largest in U.S. history. It was a mixed blessing:

On one hand, it prevented a government shutdown. The U.S. was just weeks from hitting the “X-date” in August, the day the government would run out of cash to pay its bills.

On the other hand, it opened the door to more borrowing and spending, removing one of the last guardrails of fiscal discipline.

Credit agencies and market leaders took notice. Moody’s downgraded U.S. credit one notch below AAA. And JPMorgan’s Jamie Dimon warned that bond markets could “have a tough time” absorbing this much new debt without demanding higher interest rates.

In other words, the debt ceiling increase bought time, but at a cost.

The Long-Term Cost of Rising Debt

America’s rising debt is more than a short-term refinancing challenge. It threatens to shrink the economy, crowd out private investment, reduce jobs and wages, and inject volatility into financial markets for decades to come. All as interest costs soar.

6

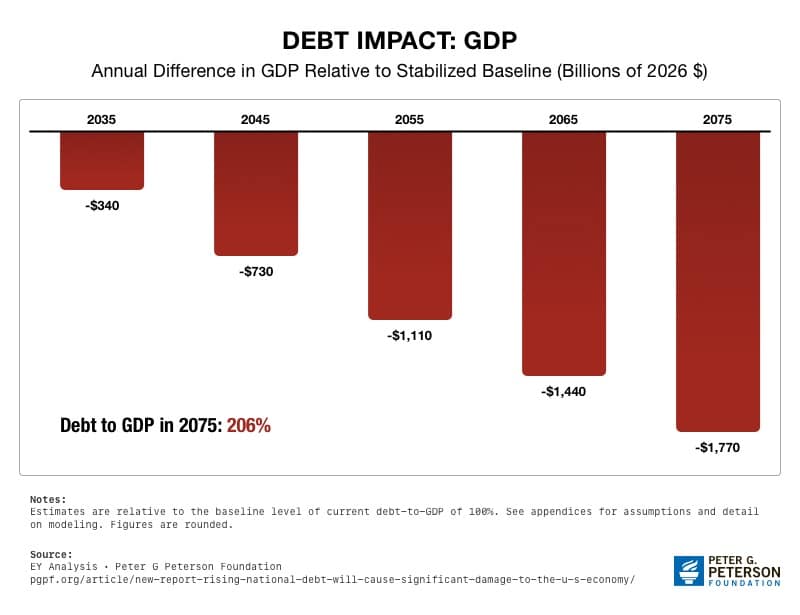

A recent analysis quantifies the damage if the current debt trajectory continues:

- S. GDP will shrink by $340 billion in 2035, $1.1 trillion in 2055, and $1.8 trillion in 2075.

- Job losses will mount, with 1.2 million fewer jobs by 2035, 2.7 million by 2055, and 3.6 million by 2075.

- Private investment will fall sharply, dropping 13.6% in 2035, 17.1% in 2055, and 21.6% in 2075.

- Wages will decline, with effective take-home pay 0.6% lower by 2035, 3.0% lower by 2055, and 5.3% lower by 2075.7

In short, the debt Americans are racking up today could weigh down the economy, jobs, and household incomes for generations. While making retirement savings more vulnerable to market swings.

Higher interest costs and market uncertainty can eat away at 401(k)s, IRAs, and other portfolios that rely heavily on equities and bonds.

Conclusion

America is crashing into a $40 trillion refinancing wall, leaving economic damage from maturing debt and rising rates in its wake. The record $5 trillion debt ceiling increase may have prevented a short-term crisis, but it did nothing to solve the long-term problem.

The writing is on the wall. Markets may face severe turbulence as the U.S. navigates this unprecedented wave of debt. History shows that holding physical gold can help protect wealth when debt and market risks collide, especially when held in a Gold IRA. To learn more, contact American Hartford Gold today at 800-462-0071.