- Private investors hold more gold than central banks, making them a major force in the gold market.

- Inflation, currency concerns, geopolitical instability, and tokenized gold are driving new private-sector demand.

- Owning physical gold in a Gold IRA can help protect your finances as you stay closer to the source of value.

Private Gold Demand Accelerates

Gold has been sought after for more than 5,000 years. From Egyptian pharaohs to Roman emperors to modern investors, gold has remained one of the world’s most trusted stores of value. Today, nearly 220,000 tonnes of above-ground gold exist worldwide, with an estimated value of about $47 trillion.1

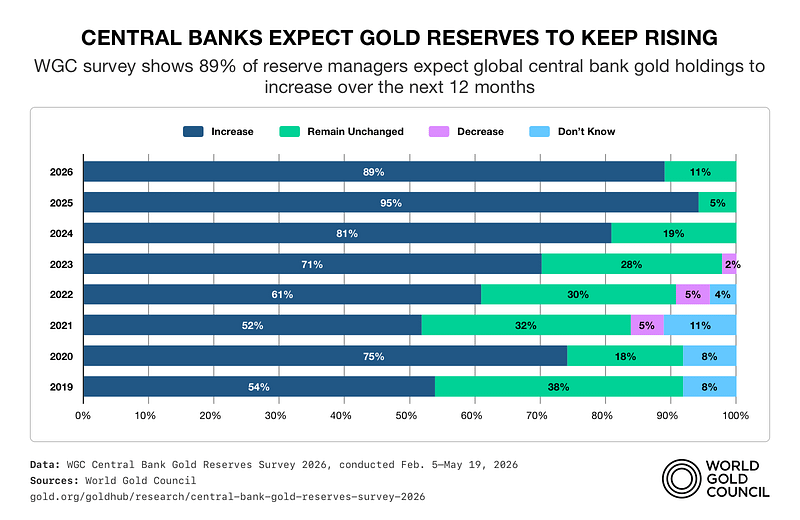

Central banks continue to play an important role in the gold market. They bought 863 tonnes in 2025, helping provide stability and a stronger foundation for prices. But the larger story is unfolding in the private sector. Individual investors are looking for protection against inflation, currency weakness, and global uncertainty. With sweeping technological revolutions and financial innovation, gold’s role as a trusted asset remains unchanged.

Private Investors Hold the Majority and Are Buying More

Private investors already hold a major portion of the world’s gold. Privately held bars, coins, ETFs, and tokenized gold account for about 38 percent of above-ground supply, or roughly 83,779 tonnes. Governments hold about 25 percent, or approximately 55,267 tonnes. Jewelry and other non-investment uses account for the remaining 37 percent. Private investors now hold about 1.5 times more gold than all central banks combined.2

Private demand is accelerating quickly. According to the World Gold Council, investment demand surged 84% in 2025 to 2,175 tonnes. Gold ETFs added 801 tonnes in 2025, reversing four consecutive years of outflows. Gold Exchange Traded Products (ETPs) now hold over 4,000 tonnes, globally representing $650 billion in assets. Annual private demand now runs 2.5 times larger than central bank purchases. 3

Projections reinforce the trend. A moderate growth scenario puts private holdings above 51% of all gold by 2045. Meanwhile, an aggressive scenario crosses that threshold as early as 2033.

Why Private Demand Is Growing

Several forces are driving investors toward gold. Inflation remains a major concern, especially for retirement savers focused on purchasing power. Gold’s strong annual returns over the past decade have strengthened that appeal.

Currency concerns are also pushing investors toward hard assets. As confidence in paper currencies weakens, many people look for assets that cannot be printed or debased.

Geopolitical instability adds another layer of demand. Wars, trade disputes, and fractured global alliances can make traditional markets feel more unpredictable. Gold is sought as a stable safe haven.

Tokenized Gold Creates a New Demand Channel

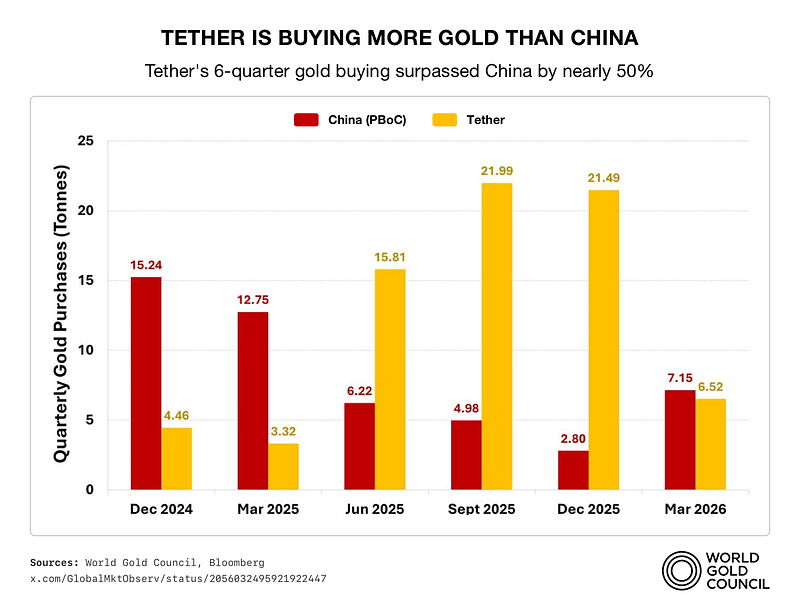

A new force is also entering the gold market: tokenized gold. Tether has become one of the first major crypto issuers to buy physical gold at scale. The company reportedly holds about 154 tonnes of gold across US Dollar Tether (USDT) reserves and its XAU₮ token, placing it among the top 30 global gold holders. They hold more gold than several countries, including Australia, Qatar, Greece, and South Korea. 4

Tether’s demand is different from traditional investment demand. The company buys gold to support its tokenized gold products. As those products grow, gold can become part of a more permanent reserve structure.

Unlike ETFs, where capital can flow out quickly, Tether’s holdings must remain in place as USDT stays in circulation. In Q4 2025, the company represented 2% of total global demand for the quarter. Analysts noted that Tether flows became a “dominant and clear driver of market behavior”. 6

CEO Paolo Ardoino has stated plans to increase gold to 10–15% of the USDT portfolio. Their gold reserves could reach 200 to 300 tonnes. Steady buying from digital asset platforms could tighten availability and create another layer of sustained demand. 7

Risks exist in this new field. But even with those risks, tokenized gold represents a meaningful new channel for private demand.

Conclusion

Central banks provide the foundation for the gold market, while private investors are building its next level. Tether and tokenized gold represent a new layer of evolution. Across all three, the story remains the same: gold is the asset that endures when other systems fail.

Its intrinsic value is tied to its scarcity. Only 3,672 tonnes were mined in 2025, reflecting modest supply growth despite high prices. Demand can move quickly. Supply often cannot. 8

Even as the means of buying and holding gold evolves, the value proposition does not. Tokens, ETFs, and digital platforms may change how investors access gold, but they all point back to the same source of value: the physical metal itself. Every step away from that primary asset can add friction, complexity, and risk. Which is why many Americans choose to stay closer to the source by owning physical gold.

Gold has survived empires, currencies, financial crises, and market cycles. As investors face inflation, debt, volatility, and geopolitical risk, the value of owning physical gold becomes even more apparent.

If you want to protect your portfolio with physical precious metals in a Gold IRA, contact AHG today at 800-462-0071.