A New Shadow Threat Emerges

In 2008, the world watched as subprime mortgage debt collapsed, taking down major banks and wiping out trillions in household wealth. What began as a problem hidden inside complex loan packages quickly became a global financial crisis. Today, a new form of shadow lending is growing in the same dark corners of finance. And many economists fear it could lead to a repeat performance.

How Collateralized Debt Fuels Hidden Risk

Private credit refers to non-bank firms that lend directly to companies. It sounds simple, but the structure behind those loans is anything but. These firms package and collateralize different forms of debt. That includes auto loans, medical bills, trade receivables, even AI-equipment leases. Then they use that collateral to raise more financing. In 2008 the underlying assets were subprime mortgages. Now they are business loans and consumer debts. They are bundled and resold in ways that few outside the system can see. When that collateral is misvalued or used to back more than one loan, it amplifies the risk to many lenders.

The Regulatory Gap That Let It Grow

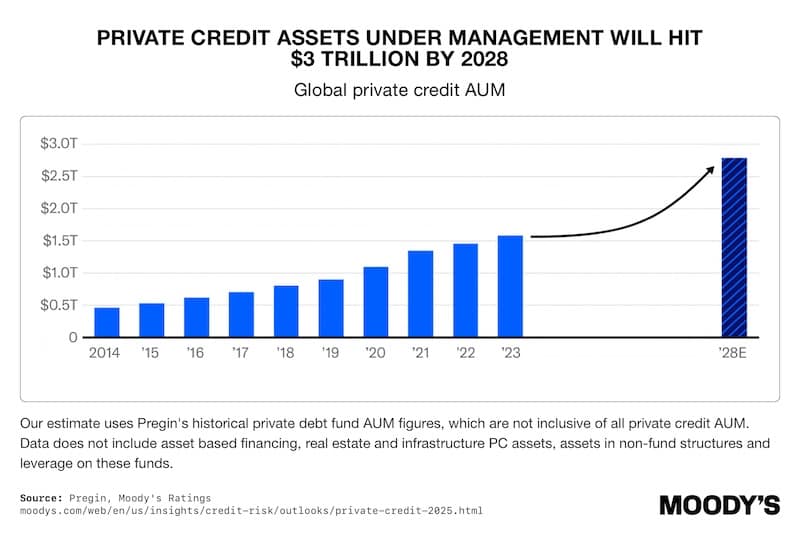

After the last crisis, Congress passed the Dodd-Frank Act. It imposed tighter oversight on banks. Regulators limited the kind of risky lending that nearly destroyed the economy. But private credit firms, which are not banks, largely escaped those rules. Over the past fifteen years, this unregulated market has ballooned. It is roughly two trillion dollars in the United States and around three trillion globally. These lenders promote their flexibility and freedom from “bureaucratic” regulation as strengths. Yet the absence of scrutiny is exactly what alarms economists who study financial contagion.

1

Yale’s Natasha Sarin warns that private credit’s rapid, secretive expansion mirrors the pre-2008 environment. 2 Only now the risk has migrated from banks into the shadows. These private funds get their money from pensions, insurance companies, and big investors. If something goes wrong, the damage won’t stay in one place. It could spread to retirement accounts, insurance savings, and even the banks. The connections may be indirect, but they are real.

Two Bankruptcies Expose the Cracks

Recent events have already exposed cracks. In September, two auto-related companies, Tricolor Holdings and First Brands Group, filed for bankruptcy. They allegedly pledged the same assets to multiple lenders. Together they held as much as ten billion dollars in liabilities. Major banks like UBS, Jefferies, JPMorgan, and Fifth Third Bank reported large exposures tied to those loans. As one analyst put it, “Sophisticated creditors armed with advanced systems were blindsided by opaque privately structured financing arrangements.”3

The market’s response was swift and nervous. JPMorgan Chase CEO Jamie Dimon said the twin collapses “raised his antenna.” He added a chilling observation: “When you see one cockroach, there are probably more.” In other words, the failures may not be isolated. They may be early warnings of deeper structural rot.4

Global Regulators Are Sounding the Alarm

Other global voices share that concern. The head of the International Monetary Fund admitted that worries about non-bank lending keep her “awake at night.” The governor of the Bank of England called the bankruptcies a “canary in the coal mine.” These are not fringe opinions. They come from the very regulators tasked with preventing another systemic collapse.5

Lenders Quietly Brace for Turbulence

Evidence of unease is also showing up in lending contracts themselves. Banks and private funds are tightening loan agreements. They are adding new clauses that restrict how borrowers can move assets or change collateral rights. In the third quarter of this year, more loans started requiring every lender’s approval before changing who gets paid first if a company fails. When seasoned lenders start changing loan agreements to protect themselves, it shows they’re getting scared about the value of the collateral and the chance of defaults.

What it Means to Everyday Americans

For ordinary Americans, this matters more than it might seem. Many 401(k) plans and insurance companies now hold stakes in private credit funds. That means everyday savers are indirectly exposed to the same opaque assets now causing bankruptcies. The risk may not appear on a monthly statement, but it exists in the system that underpins those accounts. A sharp downturn or wave of defaults could quickly spill into retirement balances and policy payouts.

History’s Lesson: Complexity Hides Fragility

History has shown how fragile complex financial chains can be. Stricter loan rules, sudden bankruptcies, and rising anxiety among regulators all show that the financial system is preparing for trouble. If economic growth slows or default rates climb, the pressure inside this unregulated sector could ignite a chain reaction that cut retirement savings almost in half in 2008.

Conclusion

Americans cannot control how regulators respond, but they can protect what they own. Physical gold remains one of the few assets that stand outside the credit system entirely. It carries no counterparty risk, no hidden leverage, and no exposure to opaque collateral.

You can protect your funds before the next financial shock with a Gold IRA from American Hartford Gold today. Call 800-462-0071 to learn how to safeguard your retirement with real, tangible gold.